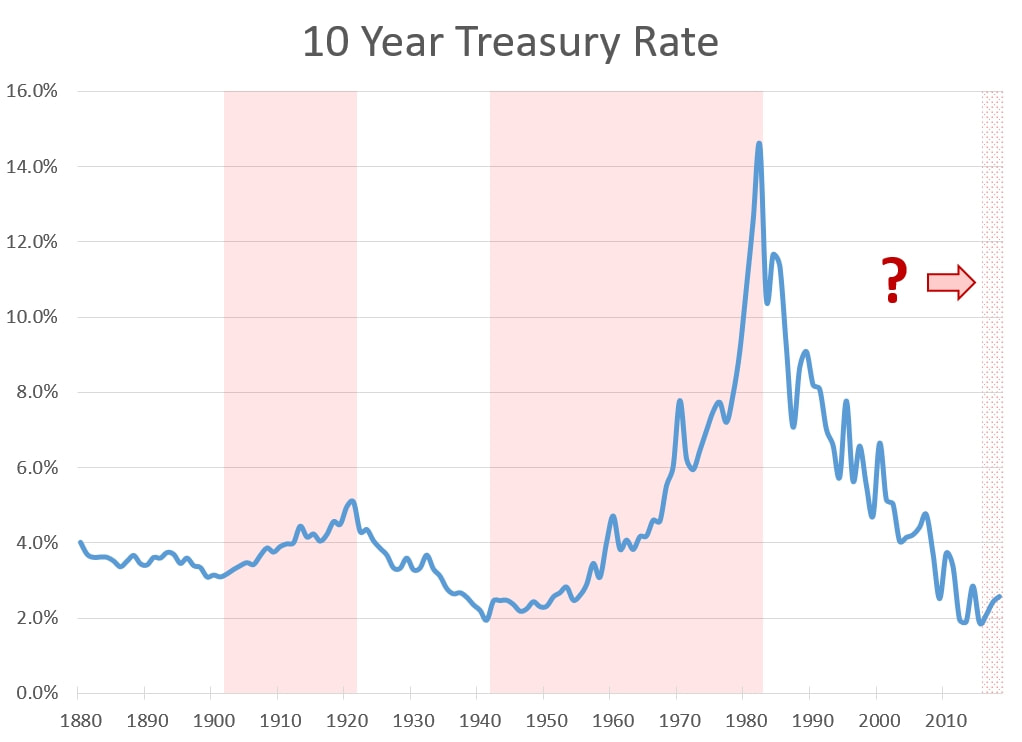

When it comes to portfolio allocation, the conventional advice is to move more of your portfolio into bonds the closer you get to retirement. "Bonds are safer than stocks" goes the mantra. After all, what makes bonds "safe" is that you receive a guaranteed rate of interest and you get paid before stockholders do if the company goes belly-up. And for those that prefer bond mutual funds, they supposedly fluctuate less than equity (stock) funds. Bonds and bond funds are therefore supposed to cushion the risk of a stock market crash. In this article, I will talk about how blindly following this advice can be dangerous to your portfolio. Over the last thirty years or so, we have been fortunate enough (in the United States) to have lived through a period of declining interest rates. This has had a beneficial effect on all things that have to do with debt... such as bonds and the real estate market. Why? Interest rates and bond prices have an inverse relationship. When rates go up, bond prices go down. Conversely, if rates go down, bond prices go up. Let's say you have a bond that will pay you $10,000 in ten years. The interest rate is 5%, so you buy it for $6,139.13. Let's say you need to sell it next year. In this first scenario, interest rates are unchanged next year, so that means you can sell it for $6,446.09 (the purchase price plus a year at 5%). In the second scenario, instead of the rates being unchanged, they went down to 2.5%. You don't have to settle for the same price as the first scenario when everything else on the market yields much less. You can now sell it for $8,007.28 so that the buyer will get $10,000 in 9 years based on current rates. That's now a 30% gain for you, as opposed to just 5%. In the third scenario, rates went up to 10% in Year 2. Nobody will want to buy your bond earning 5% when they can get one that earns 10% instead. You will have to sell it at a discount. For the math to work, you will now have to sell it at $4,240.98. That's a 31% loss! You can do the math yourself and see that the further away maturity is, the greater the loss (or gain). Sure, you can say that for the third scenario you can just hold the bond til maturity and not lose money. But you still underperformed. And what if inflation over the holding period is higher than your interest rate? If this kind of thing happens in a bond fund, the value of its assets go down, losing you money. This is called interest rate risk. The longer the term on the bonds, the greater the effect (up or down). If your bond matures next year, it's not that big of deal since you can just hold it and buy a higher yielding one next year. But if you have twenty years to go on your bond that's yielding 3% while current rates are 10%, you have problems. Let's take a look at the history of interest rates in the United States dating back to 1880.  Data as of October 12, 2018. Source: www.multpl.com Notice how interest rates rise and fall in cycles that last for decades. Notice how the last thirty years or so saw interest rates on the Ten Year Treasury Note decline from their peak in the 1980s to where they are today. Is this long term trend over? Are interest rates about to start a new 30 year rise? I can't predict the future, but looking at the chart, the idea that we could be at a turning point here in the late 2010's is not unreasonable. On the other hand, things could turn out like they did in Japan. In the early 90's their stock market crashed. Interest rates declined over a 10+ year period then stayed down for another 15+ years through the present day (2018/2019). At one point, they even turned negative. Nobody knows the future and the point of this article isn't to scare people from bonds, but rather to inform you of a risk that the cookie cutter financial advisor won't tell you about. I also have a feeling that since these cycles last for so long, most financial advisors who around today have never lived through the other side of the cycle. Therefore I would take their advice with a grain of salt when they say things like "bonds are safer than stocks". Here is a quote from an article in 2017 asking if bond funds are still safe when interest rates go up... "In the last 30 years, the data shows that fears of bond losses during rising interest rates are largely overblown." [Source] Of course... Now take a look at that chart again and notice where that 30 year period started. Everything debt has benefited over the last 30 years because of the falling rates. Bonds benefited. Real Estate benefited (lower mortgage rates mean you can take on a bigger mortgage, which means house prices go up). Will this continue? Image credits

2 Comments

2/26/2019 10:00:33 am

Interesting points. I've always just assumed bonds are safer, though admittedly I don't understand much about investing. I guess as I get closer to retirement (in 20-25 years) I'll have to carefully look at interest rates to determine if bonds are really the safest way to go or whether I should adjust my asset allocation myself and not rely on the experts. 2/26/2019 07:11:18 pm

Thank you for your comment. Yours was the first! Leave a Reply. |

Author

Follow me on Twitter (the Twitter icon below) to learn of new posts. ArchivesCategories |

RSS Feed

RSS Feed