I'm sure at one time or another you've heard someone say something like... "Wow! Bob's business is worth $3.5 million." or "Roger's business is no good. It loses $2 million a year!" or "Bill Gates is worth $90 million." Did you ever wonder what your net worth is? How much money you're making and what you're spending it on? Where you've been going financially over the past few years? If so, you should do an Annual Report on yourself. So what exactly is it and how do you do one? Publicly traded corporations are required to file Annual Reports on their finances. Just go to any big company's website and look around the Investor Relations section and you'll find it. It will tell you, among other things, what the company is worth (on a book value basis), how much debt it has, how much money it earns, and how much cash it brings in. Big money investors look at it to see if the company is worth investing in. An Annual Report will consist of the following three schedules:

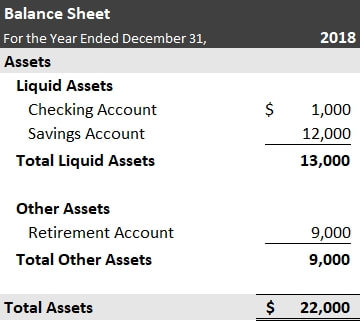

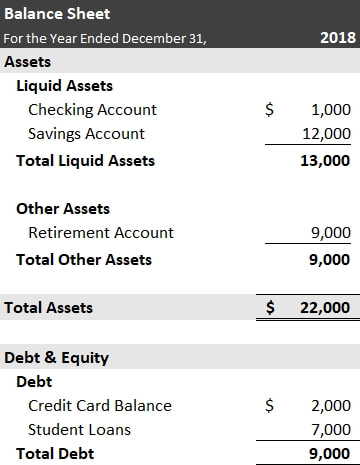

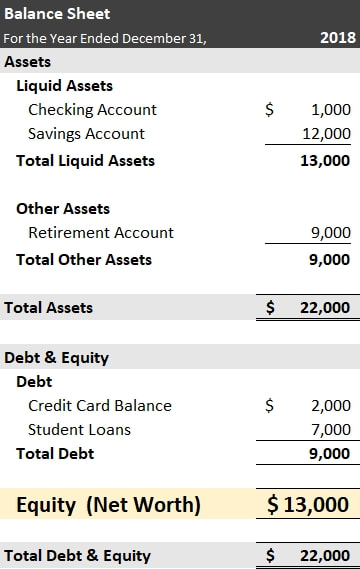

In this series of articles, I will describe each schedule, how to do one, and give a few simple examples along the way. I will wrap up the series with a more complicated and realistic example (one that includes owning a home). An Annual Report is a snapshot in time, so before we get into any specifics on what each part does, you need to decide which time period you want to do one on. I do mine as of December 31 of every year. Most people do their taxes and get their salary forms based on that date so save yourself the extra headache and just use the calendar year. The Balance Sheet he Balance Sheet is where you find out what your net worth is. To put one together you will use the following equation: Assets = Debt + Equity AssetsAssets are everything of value that you have under your name. The money in your bank account, the stocks in your investment account, your house... these are all assets. 1. Take inventory of your assets and find out their value. What was the balance of your accounts as of December 31st? How much is your house worth? etc... Write these down and come up with a total. Remember, assets have tangible value. This means things like your clothes don't belong on this list. I would even leave things like your car, furniture, and electronics off of the balance sheet. If it's something that depreciates in value once you leave the store with it, save yourself the hassle of keeping track of it. You'll probably end up throwing it out once you’re done with it anyway (except maybe your car). Here's a simple example to help you put yours together... Brian graduated from school a couple of years ago. He doesn't have enough money to own a home so he rents an apartment. On December 31, of 2018, he had $1,000 in his checking account and $12,000 in his savings account. His job offers him a 401k style retirement plan. The statement he got as of December 31st said that his account had a value of $9,000. This is what the first part of Brian's Balance Sheet will look like:  Notice how I grouped similar items together. I have a category for liquid assets (assets you can sell, spend, or get rid of quickly) and one for everything else. This distinction becomes important if you plan on doing a Statement of Cash Flows later. DebtDebt is everything of value that you owe to someone. Things like your credit card balance and your mortgage loan go in this section. 2. Take inventory of your debts and find out their value. What was the balance of your credit card as of December 31st? How much principal was left on your mortgage? etc... Write these down and come up with a total. Since Brian does not have a house, he doesn't have a mortgage to worry about either. However he did have $7,000 left to pay on his student loans as of December 31st, and his credit card balance was $2,000 as of the same date. This is what Brian's Balance Sheet looks like now:  In keeping with the format for the assets, I put the shorter term and more liquid debts first (the credit card), and the longer duration stuff (the student loans) last. EquityLastly we have equity. If you recall the equation was Assets = Debt + Equity. We already have the first two pieces, so this means that we need to plug a number in for equity so that the equation can balance out. 3. Take the total you came up with for Debt, and subtract it from your Assets. The number you get for equity is the same as your net worth. If your total debt is greater than the value of your assets, your equity (net worth) will be negative. This is the last part of the Balance Sheet. Here is Brian's:  Even though Brian has $22,000 worth of stuff, he only has a net worth of $13,000. This is because he has $9,000 worth of debt. Also notice how the $22,000 in total assets ties out to the $22,000 in total Debt and Equity. If your numbers don't tie out like this, it means that you've made a mistake somewhere. Once you can do your own Balance Sheet, anytime someone asks you what your net worth is, you can just pull up the sheet and read it off to them (or tell them to take a hike). In summary...

Image credits

0 Comments

Leave a Reply. |

Author

Follow me on Twitter (the Twitter icon below) to learn of new posts. ArchivesCategories |

RSS Feed

RSS Feed