In the first three sections of this series, I discussed the three big annual financial statements that publicly traded corporations are required to produce: the Balance Sheet, the Income Statement, and the Statement of Cash Flows... and how we as individuals can do something similar for our own finances. Along the way, I also provided simple examples for Brian, a fictional recent college graduate. In this final part, I will present a more complicated and realistic example, that of a husband and wife with a house, a mortgage, a stock portfolio, and an investment property. Robert and Maria are husband and wife. In the spring of 2018, for the first time ever, they decided to do their very own Financial Statements for 2017, so they took stock of all of their assets and set out to put together a Balance Sheet. The steps:

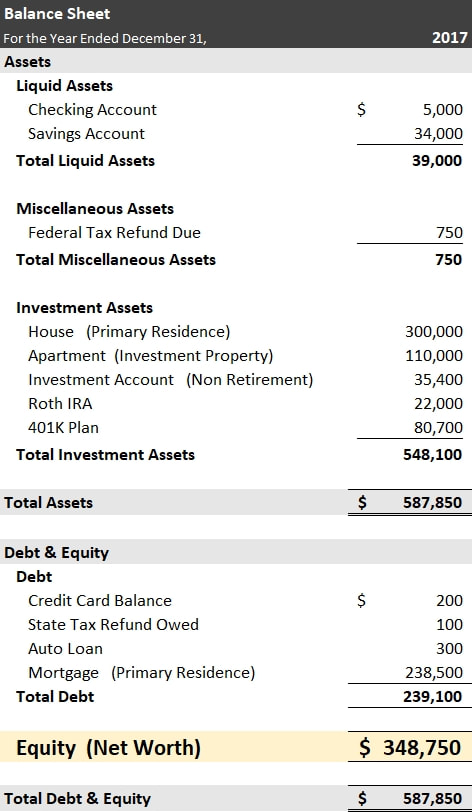

On December 31, 2017, Robert and Maria had the following:

Notice how the equation of Assets = Debt + Equity ties out. I left off the value of their car because it depreciates so fast that it's not worth putting on the statement (although you could if you wanted too). If they ever have to sell it, the money they would get would then be shown as income. Next up, they decided to do their Income Statement. Here were the steps to do one from the Income Statement article:

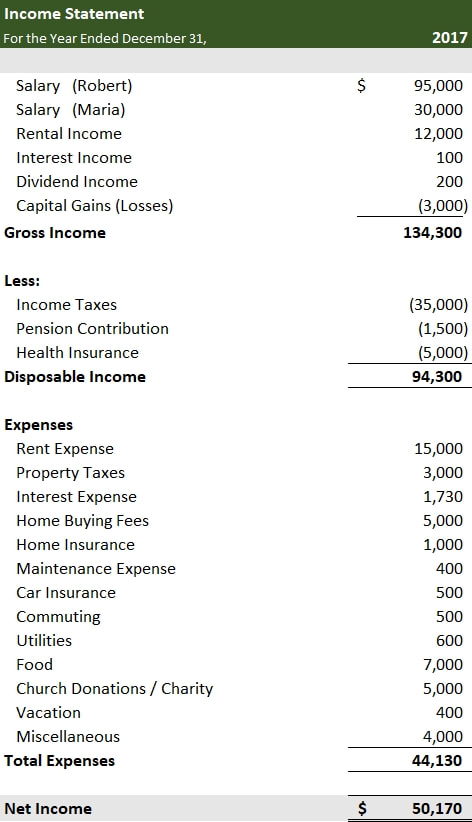

Assume every expense listed was paid off in the same year unless indicated otherwise. Here are the relevant details for 2017:

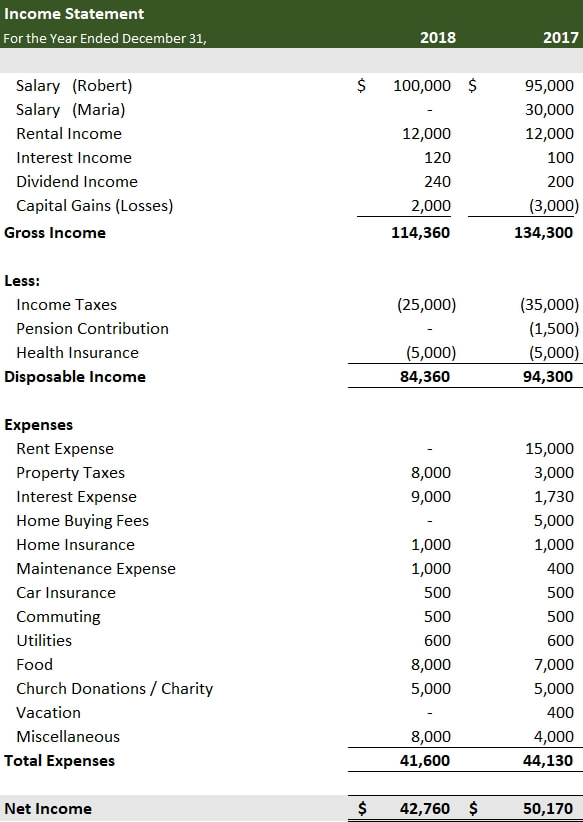

This is what their Income Statement for 2017 would look like:  Finally, they decided to do their Cash Flow statement. For reference, here were the steps from the Cash Flow article:

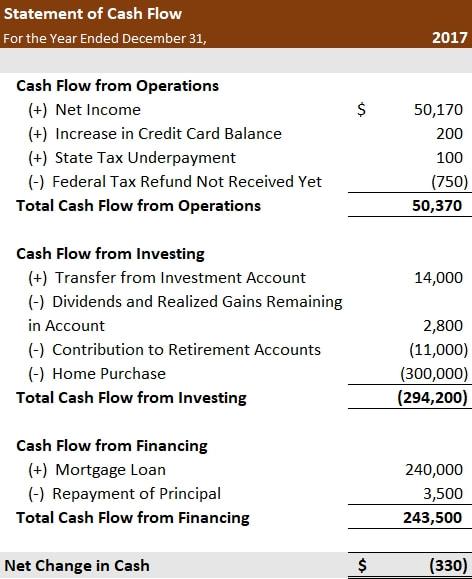

Here are the relevant details for 2017 that weren't already discussed:

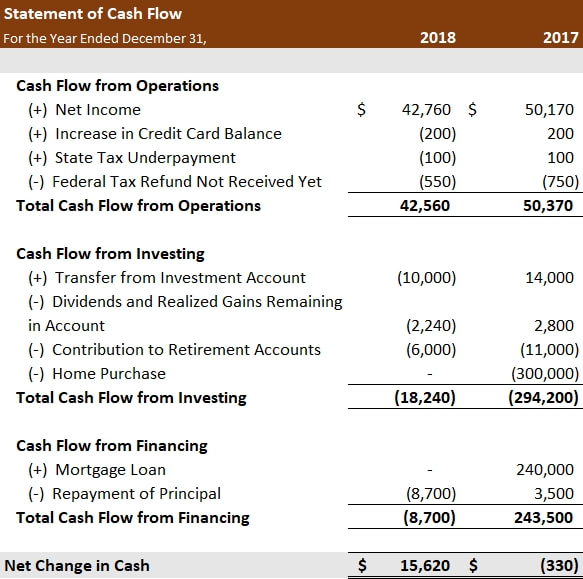

This is what their Statement of Cash Flow looks like:  Don't forget to make adjustments for the things already counted for in Net Income in 2017, but weren't paid (the cash didn't "flow out" yet). Add this stuff back... the credit card they didn't pay and the state taxes they still owe. Likewise subtract for the things already counted for in Net Income, but weren't received (the cash didn't "flow in" yet)... like their federal tax refund. Also, regarding dividends paid and realized investment gains or losses in a non-retirement account:

Notice how I netted the dividend of $200 and the capital loss of $3,000 for an addition of $2,800. Then I showed them pulling out the $14,000. You also may have noticed that I left off the following:

These things don't really affect their cash position and don't get reported on their taxes therefore it's easier to just leave them off. They work their way into the Balance sheet anyway in the form of higher account balances. Fast forward a year later... It is now 2019 and Robert and Maria are doing 2018's statements. Here is all of the relevant info:

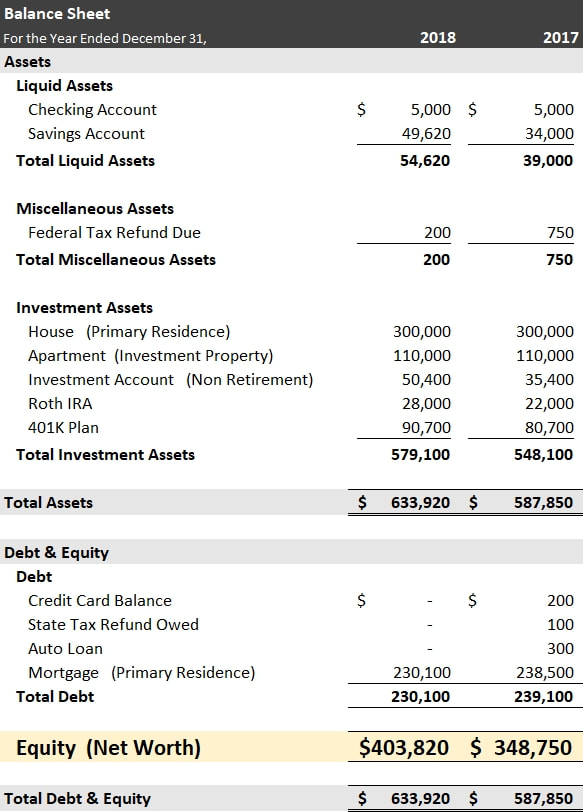

Below are all three of their Financial Statements for 2018 side by side with 2017 for comparison:    The most important thing you need to notice here is that the Net Change in Cash of $15,620 is exactly the same as the amount you would get if you took the $54,620 in 2018's Total Liquid Assets and subtracted what they had there in 2017 of $39,000. That's how you know if you did everything right. Also notice the offsetting entries in 2018's Cash Flow from Operations for their credit card balance and state tax still owed from 2017. There was also one for federal tax refund due... the reason it's $-550 instead of $-750 was because you have to add back the $200 for the refund check they won't get until 2019. And, there you have it. Hopefully this series of articles and examples didn't confuse you too much. I do these statements for myself every year and actually find it quite interesting to look at them (look at them that is, not do them, haha) and compare my situation now to what it was years ago. Hopefully you can do the same to get a sense of where you are financially right now, where you've been, and where you're headed. Image credits

0 Comments

Leave a Reply. |

Author

Follow me on Twitter (the Twitter icon below) to learn of new posts. ArchivesCategories |

RSS Feed

RSS Feed